Crypto has matured past its speculative adolescence. The 2026 M&A landscape shows fundamentally different from prior cycles. Buyers are no longer chasing narrative or token momentum. They are acquiring infrastructure, regulatory positioning, margin control, and distribution leverage.

Recent research across approximately 2,000 M&A transactions between September 2024 and March 2026 (spanning AI, crypto, fintech, and infrastructure sectors) reveals a clear pattern: crypto M&A is converging with consolidation trends seen across AI, fintech, healthcare, and enterprise software. This is not random deal flow, it is structural repositioning.

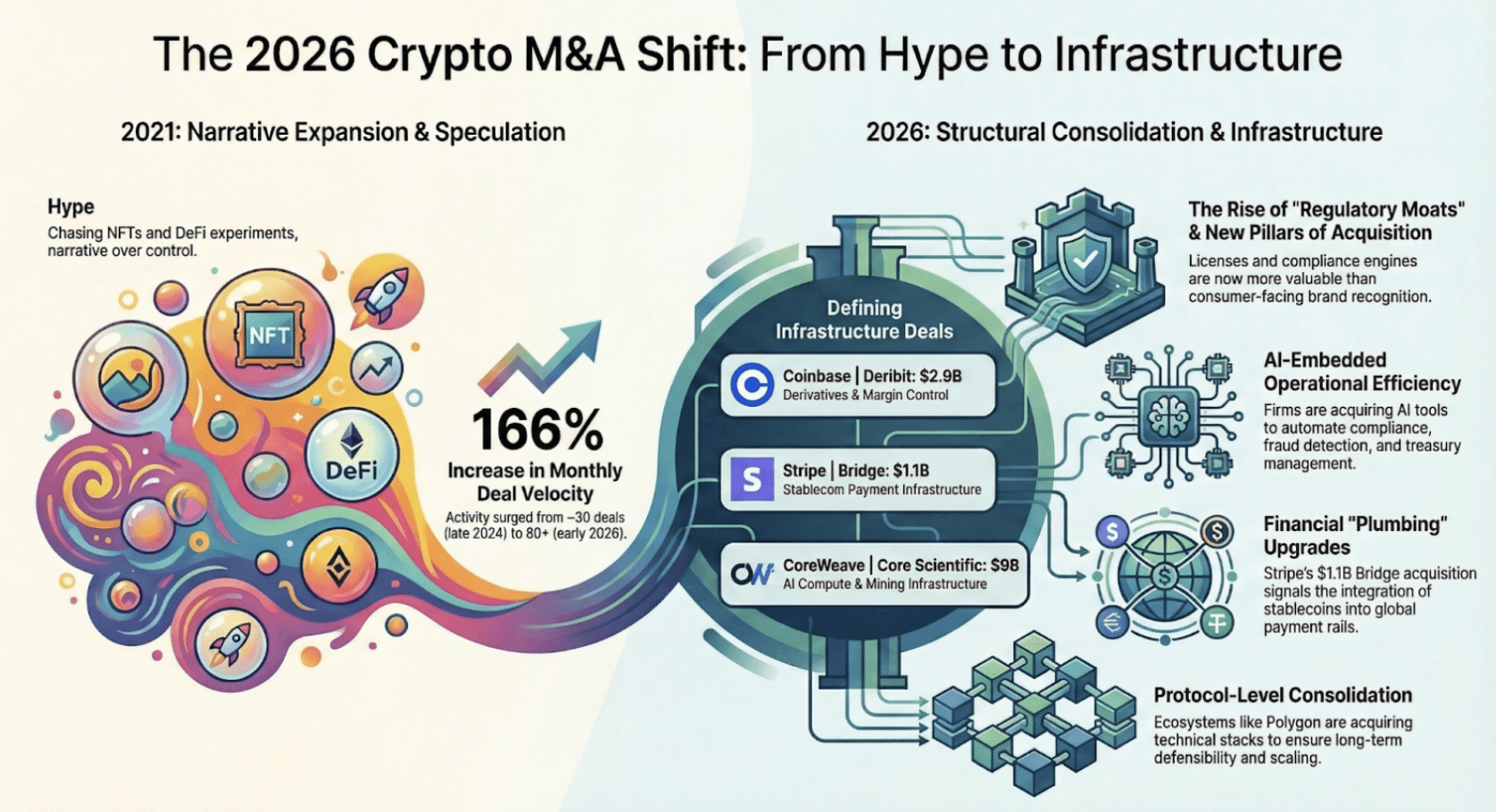

Deal velocity itself reflects this shift. Monthly deal activity across these sectors increased from ~30 deals in late 2024 to 80+ by early 2026, signaling a broader consolidation wave across emerging technology industries.

Large transactions further reinforce this transition:

Coinbase’s $2.9B acquisition of Deribit: the largest crypto M&A deal in this cycle, highlights institutional appetite for derivatives infrastructure and trading margin control.

Stripe’s $1.1B acquisition of Bridge reflects traditional financial players integrating stablecoin and crypto payment infrastructure into global payment rails.

Fireblocks’ acquisition of Tres Finance shows institutional custody providers expanding into automated credit and liquidity infrastructure.

These deals signal a structural shift: crypto infrastructure is being absorbed into the broader financial system.

From Speculation to Structural

The priorities of crypto buyers have changed dramatically since the previous cycle.

2021–2023: Narrative Expansion

Earlier M&A activity focused on growth metrics:

Token ecosystems

User acquisition

NFT marketplaces

DeFi experimentation

Ecosystem expansion

Acquirers were often chasing narrative momentum.

2024–2026: Infrastructure Consolidation

Today’s buyers prioritize defensibility and operational control. Across sectors, acquisition targets increasingly focus on:

Regulatory and compliance infrastructure

Margin consolidation through vertical integration

Institutional distribution channels

Embedded AI automation

Control over liquidity and execution layers

Crypto companies increasingly behave like financial institutions, SaaS platforms, and infrastructure providers, while traditional incumbents quietly absorb crypto capabilities into their existing operations.

Major M&A Themes Shaping Crypto in 2026

Analysis of recent deal activity reveals five structural themes shaping buyer behavior.

Financial Infrastructure Integration

Financial services remains the most structurally aligned sector with crypto M&A.

Observed patterns include:

Wealth and insurance platform roll-ups

Banks acquiring compliance and fraud technology

Private credit platform expansion

Embedded fintech infrastructure inside traditional finance

Crypto-specific acquisition priorities include:

Regulated custody infrastructure

Compliance automation (KYC, AML, identity verification)

Risk analytics and fraud detection

Lending and credit underwriting engines

Stablecoin payment rails

Key Deals

Coinbase / Deribit: derivatives infrastructure consolidation

Stripe / Bridge: stablecoin payment rails entering traditional finance

Fireblocks / Tres Finance: liquidity and credit automation

These acquisitions represent financial plumbing upgrades, not speculative bets.

Targets are often niche infrastructure startups, compliance SaaS, liquidity engines, and lending platforms, rather than consumer-facing crypto brands.

2. Artificial Intelligence Embedded in Crypto Infrastructure

AI M&A across the broader technology sector has shifted away from foundation models toward vertical integration into operational workflows.

Large companies are acquiring:

Vertical AI tools

Data infrastructure

Workflow automation platforms

Crypto firms are following the same playbook. AI capabilities being integrated include:

AI-driven compliance monitoring

Fraud detection and transaction surveillance

Market surveillance automation

On-chain analytics

Risk modeling for trading and lending

The goal is operational automation. Crypto companies are not acquiring AI research labs. They are acquiring AI tools that plug directly into trading, custody, compliance, and treasury management systems.

3. Software, Identity, and Security Infrastructure

Enterprise software consolidation is also influencing crypto M&A.

Across technology markets:

Cybersecurity acquisitions remain persistent

Vertical SaaS specialization continues

DevOps and cloud infrastructure deals remain active

Identity management tools are increasingly strategic

For crypto firms, these capabilities are foundational. Common acquisition targets include:

Identity verification systems

Wallet infrastructure providers

API and developer infrastructure

Security audit platforms

Cloud-native scaling infrastructure

Example: Protocol-Level Consolidation

Blockchain ecosystems themselves are now consolidating technical capabilities.

Polygon Labs, for example, has executed multiple acquisitions to expand its infrastructure stack and developer tooling. These moves reinforce a broader trend: protocol teams are increasingly acquiring core technology instead of building every layer internally.

The objective is ecosystem defensibility.

4. AI + FinTech Convergence

One of the most powerful cross-sector trends is the convergence of AI and financial services.

Across the enterprise landscape, AI is being deployed to:

Automate underwriting

Improve fraud detection

Optimize portfolio risk models

Enhance liquidity management

Crypto-native applications include:

Automated treasury management

Smart routing and execution optimization

Stablecoin risk monitoring

AI-driven portfolio rebalancing

Liquidity provisioning optimization

The typical acquirers in this category include:

Crypto exchanges

Institutional trading desks

Stablecoin issuers

Digital asset asset managers

FinTech infrastructure providers

These capabilities transform crypto from speculative trading infrastructure into programmable financial automation systems.

5. Infrastructure, Compute, and Industrial Signals

Crypto infrastructure is increasingly intertwined with broader industrial trends.

Large deals in adjacent sectors, including semiconductors, energy, and compute infrastructure, highlight macro positioning.

Examples include:

CoreWeave’s $9B acquisition of Core Scientific, linking AI compute demand with crypto mining infrastructure

Marvell’s $3.25B acquisition of Celestial AI, reflecting the strategic importance of AI hardware infrastructure

Implications for crypto include:

Mining economics tied to AI compute demand

Blockchain nodes increasingly competing for data center resources

Hardware supply chains influencing blockchain infrastructure

Crypto is no longer isolated from industrial cycles. It is becoming part of the broader compute and financial infrastructure stack.

What Buyers Are Actually Looking For in Crypto 2026?

Across these categories, priorities converge on:

Regulatory Moats: Licenses, compliance engines, identity infrastructure, and regulatory reporting systems are increasingly valuable.

Margin Control: Vertical integration of custody, routing, clearing, and execution layers helps protect trading margins.

AI-Embedded Efficiency: Automation of compliance, fraud detection, and liquidity optimization reduces operational cost.

Distribution Expansion: Access to institutional clients, banking partnerships, and wealth management channels is a major acquisition driver.

Capital Leverage: Lending platforms, stablecoin issuance, and credit systems provide leverage across crypto financial markets.

Speculation is no longer the driver. Defensibility and efficiency are.

If Fireblocks represents institutional consolidation, Polygon Labs represents protocol-level consolidation. By acquiring multiple companies in quick succession, Polygon signaled urgency in owning critical layers of its ecosystem, from scaling infrastructure to developer enablement. This is less about expansion and more about strategic reinforcement.

Structural Shifts Driving the M&A Cycle

Several macro-level trends are shaping buyer behavior:

Financial System Modernization: Banks increasingly acquire crypto infrastructure rather than building it internally.

Institutionalization of Crypto Markets: Derivatives, stablecoins, and custody infrastructure are becoming core institutional tools.

AI Infrastructure Consolidation: AI capabilities are being absorbed into financial systems and operational tooling.

Margin Compression: Exchanges and financial platforms face increasing competition, pushing them toward vertical integration.

Multi-Chain and Interoperability Strategies: New crypto projects increasingly launch across multiple ecosystems rather than committing to a single chain, increasing demand for interoperability infrastructure.

The Strategic Takeaway

The 2026 crypto M&A cycle is not about expansion into new narratives. It is about:

Absorbing critical infrastructure

Locking in compliance capability

Automating margin

Controlling execution layers

Securing distribution

The most attractive acquisition targets are often not the loudest, they are bottlenecks:

Identity & Risk

Liquidity routing

Compliance automation

AI-driven monitoring

Institutional onboarding rails

Crypto has entered its consolidation phase. The next generation of winners will not necessarily be the fastest builders or the loudest innovators. They will be the companies that control the rails that everyone else must use.

And that is exactly what buyers are shopping for in 2026.

Explore More Reports

Discover additional insights and strategies across AI, growth, and M&A.