The infrastructure through which users discover, evaluate, and act on information has been fundamentally rewired. The operational response is not a content refresh, it is a structural rebuild.

The Model That Built the Last Decade Is Breaking

The attention economy trained operators to compete on surface area: more pages, more backlinks, more spend, more output.

Traffic was the currency. Platforms were the rails. That model became doctrine.

That doctrine is now a liability. Search is no longer a gateway. It’s increasingly the endpoint. Organic CTR on queries with AI Overviews dropped 61% (Seer, 25M+ impressions). 60% of all Google searches now end without a click to any website, up from roughly 25% a decade ago.

Meanwhile, LLM adoption among enterprises has reached an inflection. McKinsey's 2024 Global Survey on AI found that 65% of organizations regularly use generative AI, nearly double the 33% figure from ten months earlier. In the 2025 edition, 23% of organizations are already scaling agentic AI systems, with another 39% actively experimenting. These are not experimental budgets. They are structural reconfigurations.

The argument here is not that marketing is dead. It is that the discipline as most organizations currently practice it: campaign-centric, channel-centric, traffic-obsessed, is being made obsolete by a shift in how information flows. The Retrieval Economy is not a trend. It is the new operating environment.

The Macro Shift: From Attention to Retrieval

The attention economy was legible. You could model it: impressions led to clicks, clicks led to conversions, conversions funded more impressions. The key inputs were distribution (platform algorithms) and content (the product you pushed through them). Optimization was competitive but tractable.

The Retrieval Economy operates differently. Users don’t navigate. They summon.

The interface is a query. The output is an answer. And increasingly, the "user" issuing that query is not a human at all, it is an AI agent acting on a human's behalf.

The search box was a voting machine. The LLM query is a judgment call. One returns options; the other returns decisions.

This shift is visible in the data. Perplexity AI processed roughly 780 million queries per month as of mid-2025, up from 230 million just nine months earlier, a 239% increase. OpenAI grew from $2B ARR in 2023 to $20B+ in 2025, scaling 10x in two years by embedding its models across developer workflows, enterprise stacks, and consumer surfaces simultaneously.

60% of all Google searches now end without a click to any external website Onely / SparkToro / Similarweb, 2025 239% increase in Perplexity AI monthly query volume in under 9 months (Aug 2024 to May 2025) Backlinko / Perplexity, 2025 |

The shift is simple: as the cost of synthesis collapses, the value of curation rises.

For years, users navigated because they had to. Now they don’t.

The question is no longer "which link should I click?", it is "what does the most trusted synthesis say?"

Dimension | Attention Economy | Retrieval Economy |

User Behavior | Browse, click, compare | Query, receive, act |

Discovery Layer | Search engines, social feeds | LLMs, AI search, agents |

Content Role | Source of traffic | Training signal & citation substrate |

Growth Moat | Domain authority, ad budget, backlinks | Structured knowledge, citability, trust |

Primary "User" | Human, browsing manually | AI agent, operating autonomously |

Distribution Channel | Platform placement (SEO, PPC, social) | API integration, system-level embedding |

Content Evolution: From Content to Structured Knowledge

The content marketing playbook: publish frequently, rank for long-tail keywords, build topical authority was designed for a world in which Google's ranking algorithm was the primary gatekeeper. That algorithm rewarded volume, freshness, and backlink density. Entire industries were built around gaming it.

LLMs are a different kind of gatekeeper. They do not rank. They retrieve, synthesize, and cite. LLMs don’t reward freshness or backlinks. They reward structure, clarity, and trust.

The implicit question: can this be cited? Most content marketing output cannot answer yes. The evidence of this transition is already punishing. HubSpot’s organic traffic dropped from ~13.5M to under 7M in months. HubSpot's CEO acknowledged directly on an earnings call that "AI overviews are giving answers, and fewer people are clicking through to websites." Chegg reported a 49% decline in non-subscriber traffic over the same period. These are not edge cases. They are early signals of a structural repricing of content as an asset class.

Example: Reddit & the Structured Signal

While most publishers lost traffic, Reddit's grew to 1.4 billion monthly visits by April 2025. The reason matters: Reddit's conversational, experience-anchored content aligns precisely with what LLMs seek: authentic, opinionated, verifiable-by-experience human knowledge. It is structurally citable in ways that optimized blog content is not. Reddit also holds a data licensing deal with Google, formalized in February 2024, which enhanced its visibility in AI-generated responses. The lesson: the format and provenance of knowledge matters more than its volume.

The strategic implication is not to abandon content. It is to redefine what content means. Structured knowledge: well-sourced, schema-marked, factually dense, semantically organized, gets retrieved. SEO-optimized prose gets ignored. Organizations that treat their intellectual output as a retrievable knowledge asset rather than a traffic-generation engine will have a structural advantage.

This includes: building authoritative knowledge bases with explicit source attribution; structuring output with semantic markup (Schema.org, FAQ schema, entity-level structuring); and prioritizing depth over breadth of fewer, definitive pieces rather than high-frequency shallow coverage. Research shows that 96.55% of content receives zero organic traffic from Google in the current environment. The long tail is not just diminishing, it is functionally worthless in a retrieval-first world.

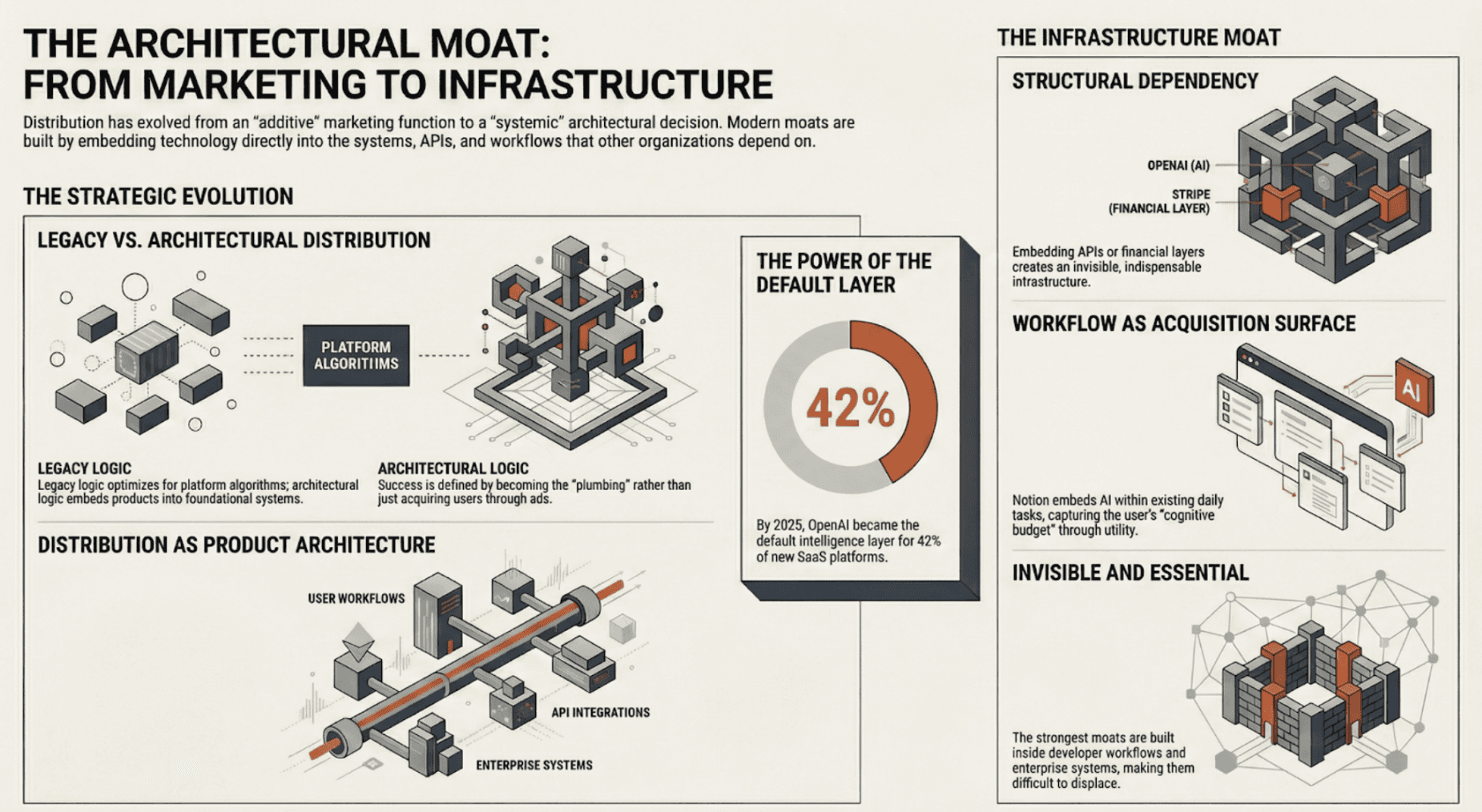

Distribution Evolution: From Platforms to Systems

Legacy distribution logic is additive: more channels, more placements, more reach. Platform algorithms determined visibility, so operators optimized for platforms. The risk was concentration, over-reliance on Google, Facebook, or LinkedIn, but the model was at least comprehensible.

AI-era distribution is architectural. It happens at the system level, not the placement level. The winners aren’t running better content calendars. They’re embedded in the systems others depend on.

Example

OpenAI: The API as Distribution

OpenAI's most durable competitive advantage is not ChatGPT as a consumer product. It is the API. OpenAI grew from $2B ARR in 2023 to $20B+ in 2025 but the more significant metric is that by early 2025, over one million organizations had embedded OpenAI's technology into their stacks. When your model is the default intelligence layer across 42% of newly launched SaaS platforms with AI components, distribution becomes a function of infrastructure not marketing. You are not acquiring users. You are becoming the plumbing.

Example

Stripe: Embedded Infrastructure as Moat

Stripe did not grow by running performance campaigns. It grew by becoming the default financial infrastructure for developers. Every startup that integrated Stripe became a distribution node: Stripe's product sat inside their checkout, exposed to every transaction, every operator, every downstream user. The moat was not brand awareness, it was structural dependency. The same logic now applies to AI. The companies that embed their models, knowledge bases, or capabilities into developer workflows and enterprise systems are building Stripe-style distribution: invisible, essential, and extremely difficult to displace.

Example

Notion: Workflow as Acquisition Surface

Notion's AI integration did not enter a market, it colonized an existing one. By embedding AI capabilities inside a tool millions already use for daily workflows, Notion made its product the natural interface for AI-assisted knowledge work. Its distribution advantage is the workflow itself: every document created, every knowledge base updated, every meeting note processed becomes a surface for AI-delivered value. Workflow integration is the new homepage. The brand that operates inside your workflow owns more of your cognitive budget than any ad campaign ever could.

The strategic reframe here is from distribution as a marketing function to distribution as a product architecture decision. Operators need to ask: where do our users or the systems acting on their behalf already spend time? And how do we build our product to be structurally present there?

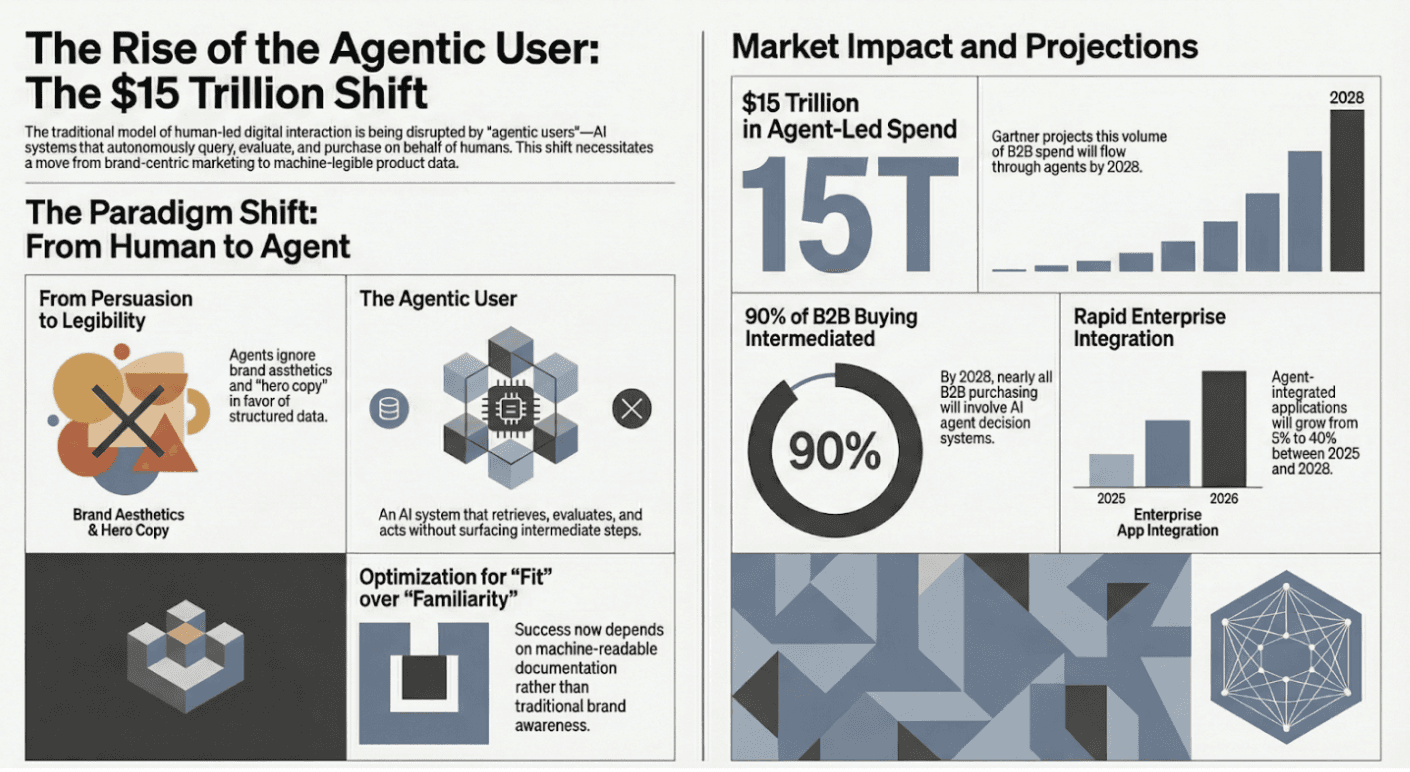

The Agent Layer: AI Agents as the New Users

This is the most underpriced shift in the current landscape. When operators think about users, they think about humans. A human visits a site, reads a page, and makes a decision. Every piece of marketing infrastructure from ad copy to landing page design to CRM workflows is built for that model.

That model is being structurally disrupted. Increasingly, the "user" making the first-touch interaction with your product or content is not a human. It is an AI agent acting on a human's behalf. That agent does not browse. It queries, retrieves, evaluates, and acts, often without surfacing its conclusions to the human until a decision has already been made.

Gartner projects that 40% of enterprise applications will be integrated with task-specific AI agents by the end of 2026, up from less than 5% in 2025. In their Strategic Predictions, Gartner forecasts that by 2028, 90% of B2B buying will be AI-agent intermediated, pushing over $15 trillion of B2B spend through agent-driven decision systems. These are not incremental projections. They represent the wholesale displacement of human judgment at the top of the purchase funnel.

$ 15T in B2B spend projected to flow through AI agent decision systems by 2028, per Gartner's Strategic Predictions framework Gartner Strategic Predictions for 2026 and Beyond |

The implications for go-to-market strategy are significant. If the primary evaluator of your product, pricing, and positioning is an AI agent then the traditional levers of awareness and persuasion become secondary. What matters is whether your product is structured to be legibly evaluated by a system that cannot be charmed, persuaded, or brand-impressed. Agents optimize for fit, not familiarity.

Concretely: if an AI procurement agent is comparing three vendors for a CFO, it will query structured knowledge sources, API documentation, case study databases, and third-party review platforms. It will not read your homepage hero copy. Organizations that have invested in structured, machine-readable product and pricing information will be surfaced. Those that have invested primarily in brand aesthetics will not.

McKinsey's 2025 State of AI report notes that agentic AI use is most concentrated in IT and knowledge management, where deep research and service-desk automation are the leading applications. But the trend is directional: as agent capabilities mature, their domain of action expands. The operators who build agent-legible products today will have a structural advantage when agents become the primary buyers in their category.

The New Moat

Trust & Citability as Durable Advantage

In the attention economy, the growth moat was distribution: whoever could acquire traffic cheapest, at scale, won. In the Retrieval Economy, the moat is something harder to build and harder to replicate: epistemic authority. The question is not whether your content can be found, it is whether it can be trusted, by both human readers and by the AI systems that synthesize on their behalf.

The data is unambiguous on the commercial value of citability. Seer Interactive's September 2025 research found that brands cited in Google AI Overviews earn 35% more organic clicks and 91% more paid clicks than uncited brands on the same queries. Being cited is not just a visibility play, it is a compounding trust signal. AI systems cite sources that have been cited before. The rich get richer, but the currency is credibility, not ad budget.

In the attention economy, the question was: how do I get in front of the user?

In the Retrieval Economy, the question is: does the system trust me enough to surface me?

The mechanism for building this kind of trust is different from traditional brand building. It requires: consistent factual accuracy across published claims; clear attribution and sourcing practices; domain-specific depth rather than generalist coverage; and structural alignment with how AI systems parse and evaluate information which means explicit entity definitions, named sources, consistent terminology, and verifiable claims.

The companies that understand this earliest are building what might be called citation infrastructure: knowledge bases designed not just for human readers but for machine retrieval. Perplexity's model which returns sourced answers with visible citations is already conditioning a generation of users to treat citability as a proxy for quality. Perplexity now processes approximately 600 million queries per month and maintains over 300 publisher partnerships through which it shares ad revenue. That revenue-sharing model is an early signal of how the economics of the Retrieval Economy will eventually settle: value flows to sources, not to intermediaries.

Example

Perplexity: The Retrieval-Native Product

Perplexity's growth arc is instructive precisely because it is retrieval-native by design. Unlike traditional search, it does not return a list of links, it synthesizes, cites, and attributes. This positions Perplexity as a test case for what the Retrieval Economy looks like at scale: 600M+ monthly queries, $200M ARR, $20B valuation built not on ad inventory but on the quality of retrieval. Its growth also validates the commercial thesis: users are paying for better retrieval, not better browsing. The product distinction is not convenience, it is epistemic quality.

The Operational Shift

Marketing to System Design

The practical consequence of everything above is a reconception of what the marketing function is actually for. In the Retrieval Economy, marketing is not primarily a demand-generation function. It is an information architecture function. The CMO's job is not to run campaigns, it is to ensure that the organization's knowledge, expertise, and positioning are structured in a way that retrieval systems can accurately represent.

This requires a different set of capabilities and a different operating model. The key transitions:

From SEO to GEO (Generative Engine Optimization). IDC has flagged this shift explicitly as "marketing's new imperative." GEO is the practice of structuring content and knowledge assets to be retrievable and citable by LLMs, not just rankable by traditional algorithms. It includes semantic structuring, entity disambiguation, and explicit sourcing practices.

From content calendars to knowledge architectures. The unit of publishing is no longer the blog post, it is the authoritative piece of structured knowledge. Fewer, deeper, better-sourced assets that can serve as durable citation targets outperform high-frequency content that decays rapidly in AI-mediated environments.

From brand awareness to system-level presence. The goal of distribution is not to be seen by users, it is to be embedded in the systems users rely on. This means API-first product architecture, integration with enterprise knowledge platforms, and investment in developer ecosystems.

From traffic metrics to retrieval metrics. Organic CTR, session duration, and bounce rate are increasingly unreliable measures of marketing effectiveness in a zero-click world. The metrics that matter are: citation frequency in AI-generated responses, share of voice in LLM outputs for category-relevant queries, and brand mention rate in agent-accessible knowledge sources.

From ad-driven acquisition to trust-driven distribution. a16z's 2025 enterprise AI research notes that incumbents with established trust and existing distribution are being outperformed by AI-native competitors on product quality and innovation velocity. The transition is from spending to signal: organizations that earn AI citations have lower marginal acquisition costs than those that buy ad placements because the citation compounds while the ad expires.

The organizational implication is structural. Teams built around campaign execution, paid channel management, and content volume are misaligned with what the Retrieval Economy rewards. The highest-leverage hires in this environment are those who understand knowledge graph construction, API-accessible content architecture, and AI system behavior, not growth hackers optimizing for click-through rates.

Gartner predicts that 60% of brands will use agentic AI to deliver personalized one-to-one interactions by 2028. That prediction is often read as a product roadmap item. It should be read as an organizational design imperative: the companies building those agentic systems today are assembling the knowledge infrastructure, data architecture, and integration layers that will define their distribution reach for the next decade.

Conclusion

The Retrieval Economy is not an AI story. It is a structural reorganization of how value flows through information markets. The companies that will define the next decade are not those that produced the most content, ran the best campaigns, or optimized most aggressively for platform algorithms. They are the ones whose knowledge, products, and capabilities are so precisely structured, so citable, so machine-legible, so architecturally present, that they get retrieved by default.

The shift from SEO to GEO is real but insufficient as a framework. The deeper shift is from marketing as outbound communication to marketing as system design. The question is no longer: how do we reach users?

It’s: are we embedded in the systems that decide?

Three operational conclusions for operators and advisors:

Audit your retrievability, not just your rankability. Run your own brand and product queries through Perplexity, ChatGPT, and Google's AI Mode. What gets surfaced? What gets cited? What is invisible? That gap is your strategic exposure.

Build knowledge assets, not content assets. Structured, sourced, entity-rich knowledge is what retrieval systems favor. Invest in depth, not velocity. One authoritative piece that earns citations compounds indefinitely. A hundred SEO articles optimized for 2023 are depreciating rapidly.

Design for agent-legibility. The next procurement cycle in your category may be partially mediated by an AI agent. Your pricing pages, API documentation, and case studies need to answer the questions an agent will ask: structured, factual, comparable, verifiable.

The question that defined growth in the last era was: how do I get traffic?

The question that will define growth in this era is: does the system that mediates my customer's decisions know who I am and trust what I say?

Explore More Reports

Discover additional insights and strategies across AI, growth, and M&A.